July 18, 2026 · 5 min read

3 Retirement Income Strategies From Vanguard's Latest Report

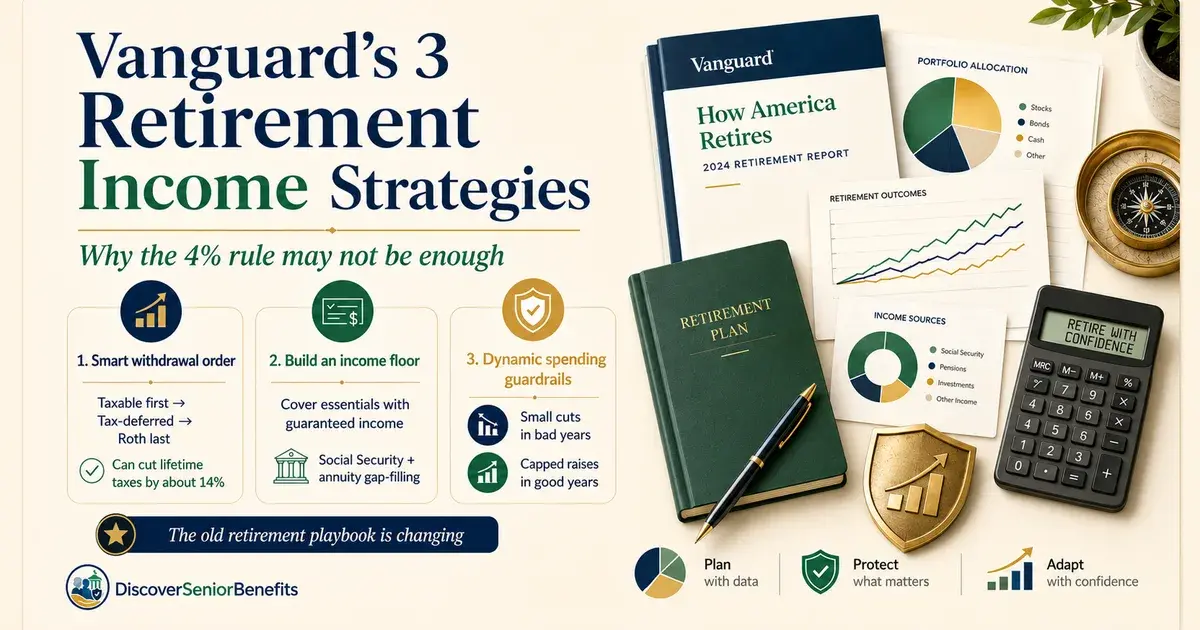

Vanguard's research goes beyond the familiar 4% rule, laying out three strategies to help retirees turn savings into lasting income — including one recommendation that surprised even longtime Vanguard followers.

Key takeaways

- Withdrawing from accounts in the right order — taxable first, then traditional IRA, then Roth last — can cut lifetime taxes by roughly 14%.

- Covering essential expenses like housing, food, and healthcare with guaranteed income (such as Social Security or an annuity) protects against sequence-of-returns risk.

- Income annuities lock in a fixed payment for life but do not automatically adjust for inflation, so purchasing power can shrink significantly over 20–30 years.

- Dynamic spending with guardrails — capping raises in good years and taking small cuts in bad years — can extend a portfolio's life and leave retirees wealthier at age 100.

- The 4% rule was always a starting point, not a guarantee; longer lifespans and volatile markets require a more flexible approach.

- Setting spending rules in advance removes emotion from the decision, protecting retirees from panic-selling during market downturns.

Why the 4% Rule May Not Be Enough

For decades, the standard retirement advice has been simple: withdraw about 4% of your savings each year, adjust for inflation, and you should be fine. That rule came from historical data and was popularized in the late 1990s. It assumes a steady withdrawal rate and that the market will generally cooperate.

But lifespans are stretching into the 90s and beyond. Markets drop 20% or more, on average, at least once every six years. A 30-year retirement means facing that kind of drop multiple times. Vanguard's research acknowledges that the 4% rule was always a starting point — not a guarantee — and that retirees today need a more adaptive income structure.

Vanguard's report lays out three strategies for turning a nest egg into income that lasts: a smart withdrawal order, an income floor built on guaranteed income, and dynamic spending with guardrails.

Strategy 1: The Smart Withdrawal Order

Most retirees pull money from whichever account is easiest to access, without thinking about the tax consequences. Vanguard's data shows that the order in which you withdraw matters — a lot.

The recommended sequence:

- Taxable accounts first (brokerage accounts, savings) — withdrawals here are taxed only on capital gains, not the full amount.

- Tax-deferred accounts second (traditional IRA, 401(k)) — this money was never taxed, so it counts as ordinary income when withdrawn.

- Roth IRA last — withdrawals are completely tax-free, and the account keeps compounding the longer it is left alone.

Vanguard modeled this against the common approach of withdrawing proportionally from all accounts at once. Same starting portfolio, same spending — only the order changed. The result: the smart order cut cumulative lifetime taxes by about 14% by age 100. On a mid-size portfolio, that can mean tens of thousands of dollars staying in your pocket instead of going to the IRS.

A common mistake is tapping the Roth early to avoid paying taxes now. But Roth money growing tax-free for 20 or 30 years can double or triple. Draining it early sacrifices that compounding permanently.

Strategy 2: Building an Income Floor for Essential Expenses

Vanguard draws a clear line between essential expenses — housing, food, healthcare — and discretionary spending like travel or entertainment. Essential expenses show up every month regardless of what the market does. Vanguard argues they should be covered by income that is equally reliable.

Social Security is the first piece of that floor. But for many retirees, it does not cover everything. If essential expenses run $50,000 a year and Social Security covers $30,000, there is a $20,000 gap. Pulling that gap from a portfolio introduces sequence-of-returns risk — the danger that a market drop early in retirement permanently damages withdrawal math.

Vanguard's surprising recommendation: consider filling that gap with an income annuity — a product that pays a fixed amount every month for the rest of your life. Their modeled example involves a 67-year-old woman with $500,000 in savings who needs $45,000 per year. Social Security covers $15,000, leaving a $30,000 shortfall. A 6% annual withdrawal rate from her portfolio carries a significant risk of running out of money, especially if markets drop in the first few years.

If she instead puts 60% of her savings ($300,000) into an immediate fixed annuity, she locks in roughly $18,000 per year for life. Combined with Social Security, that covers most of her essential spending. The remaining $200,000 stays invested and is drawn on more sustainably. Vanguard's model shows that by age 83, her total wealth is actually higher than if she had never bought the annuity — because the guaranteed floor kept her from draining the portfolio too quickly.

The Hidden Risks of Income Annuities

Before acting on the annuity recommendation, it is important to understand what Vanguard's report addresses only briefly.

Inflation erosion. Most immediate fixed annuities do not include an inflation adjustment. A $30,000 annual payment locked in today, with inflation running at a historical average of 3%, has the purchasing power of roughly $16,600 after 20 years and about $12,300 after 30 years. Healthcare costs — a major essential expense for older retirees — have historically risen faster than general inflation, widening the gap exactly when it matters most.

Loss of flexibility. Once a lump sum is handed over for an immediate annuity, that money is gone. It cannot be accessed for emergencies, left to heirs, or rebalanced if circumstances change. A major medical bill, a home repair, or a family need leaves no recourse from those funds.

Portfolio performance comparison. Vanguard's own modeling on dynamic withdrawal strategies shows that a diversified portfolio with guardrails tends to leave retirees with roughly 40% more wealth at age 100 than the annuity path, assuming average market returns. Annuities are best understood as insurance against the specific risk of living a very long life with no income left — not as a core investment building block for everyone.

Always confirm the details of any annuity contract with a qualified, fee-only financial professional before committing.

Strategy 3: Dynamic Spending With Guardrails

The third strategy is the one Vanguard's own data supports most strongly for building long-term wealth: dynamic spending with guardrails.

Instead of withdrawing a fixed dollar amount every year, you set rules in advance:

- In a good year, when the portfolio grows, give yourself a raise — but cap it (Vanguard's data suggests capping raises at around 12% above inflation). This prevents lifestyle creep from locking in a spending level that becomes unsustainable.

- In a bad year, when the portfolio drops below a set threshold, trim spending — but only modestly, perhaps 2–3%. A small, planned cut is far less damaging than the panic-driven decisions that often follow a market drop.

Vanguard modeled two retirees: one spending a flat inflation-adjusted amount every year, and one using dynamic guardrails. The flat-spending retiree looks fine through their 60s and 70s, then runs out of money around age 92 because they never adjusted during down markets. The dynamic-spending retiree makes small, manageable adjustments along the way — and at age 100, still has more wealth than they started with.

The key benefit of setting guardrails in advance is behavioral. Watching a portfolio drop $100,000 or more in a month triggers a panic response. Without a pre-set plan, retirees often sell at the worst time or cut spending far more than necessary. Guardrails replace that emotional reaction with a rule the market itself triggers — removing fear from the equation.

Putting It All Together

Vanguard's three strategies work as a system:

- Withdraw in the right order to minimize taxes over a lifetime.

- Cover essential expenses with guaranteed income — Social Security plus, potentially, an annuity — to protect against sequence-of-returns risk.

- Use dynamic spending with guardrails to let the portfolio breathe, grow, and last through a long retirement.

The deeper message from the report is that retirement income planning is not a single number or a simple rule. It is a structure — one that accounts for taxes, market volatility, longevity, and human behavior. The 4% rule was a useful starting point, but it was never designed to handle 30-year retirements, repeated market downturns, or the behavioral challenges of managing money under stress.

Building a system in advance — one that tells you exactly what to do when markets rise or fall — is what separates retirees who run out of money from those who spend confidently into their 90s and beyond. Consult a financial professional to determine which combination of these strategies fits your specific situation.

Not legal or financial advice. The agency makes the final eligibility decision.