June 8, 2026 · 5 min read

Authorized Representative vs. Power of Attorney: What Caregivers Need to Know

When helping an aging parent manage benefits, most adult children reach for a Power of Attorney first — but a simpler, faster, and free tool usually does the job. Here's how to tell the difference and use each one correctly.

Key takeaways

- An Authorized Representative (AR) designation — not a Power of Attorney — is the right first tool for managing a parent's benefits like Medicaid, SNAP, or SSI.

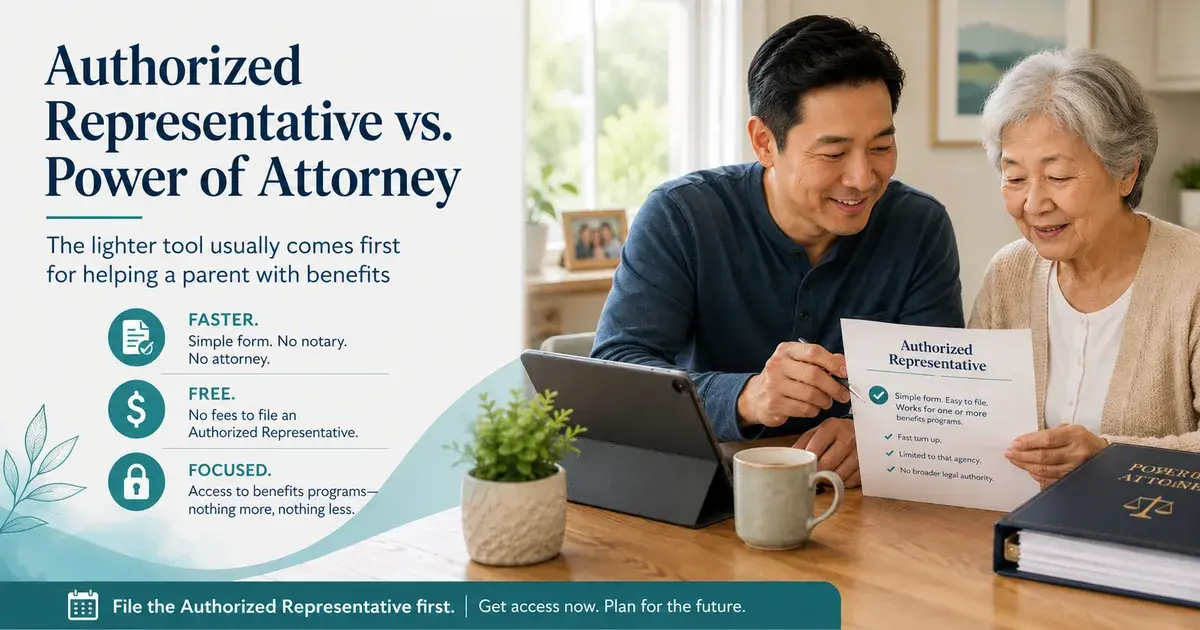

- The AR designation is free, requires no attorney or notary, and typically processes in a few business days.

- A Power of Attorney is needed for major decisions involving bank accounts, real estate, contracts, or medical care — not for routine benefits work.

- Having a Power of Attorney does NOT automatically grant AR status; the AR form must still be filed separately with each program's agency.

- An AR designation only covers the specific program it was filed for — a separate form is needed for each program, unless using an integrated state portal.

- The recommended sequence: file the AR designation in the first two weeks, then arrange Power of Attorney and advance directives in the following month.

The Common — and Costly — First Instinct

When an adult child starts helping an aging parent navigate benefits — signing up for Medicaid, renewing SNAP, or talking to a caseworker — the instinct is often to call an attorney and get a Power of Attorney (POA) drawn up right away.

This is usually the wrong first move. A POA is a heavy legal instrument built for situations where a parent can no longer make their own decisions. For day-to-day benefits work, a much lighter and faster tool almost always does the job: the Authorized Representative (AR) designation.

Knowing the difference between these two tools can save families weeks of unnecessary legal work and several hundred dollars in attorney fees.

What a Power of Attorney Actually Is

A Power of Attorney is a legal document signed by a competent adult (called the principal) that gives another person (the agent) authority to act on the principal's behalf. There are several common types:

- Financial POA — covers bank accounts, investments, real estate, contracts, and tax matters.

- Healthcare POA (also called an advance directive or healthcare proxy) — covers medical decisions when the principal cannot make them.

- Limited or special POA — covers one specific transaction, like selling a particular property.

- Durable POA — stays in effect even if the principal becomes incapacitated. A non-durable POA ends at incapacity.

POAs are drafted by attorneys or using state-approved templates, signed before a notary public, and sometimes require additional witnesses. Financial institutions, hospitals, and real estate offices each review the document on their own terms — and some have strict rules, like refusing a POA that is more than a few years old.

POAs are powerful and serious. They are the right tool for major life decisions about money, property, and medical care. But they are overkill for managing a parent's benefits.

What an Authorized Representative Is

An Authorized Representative designation is a benefits-system tool, not a legal document. The person receiving a public benefit — such as Medicaid, SNAP, SSI, or a VA pension — names another person as their AR by completing a short, program-specific form. Once filed, the AR can:

- View the recipient's case information

- Submit renewals and upload documents

- Speak with the caseworker

- Receive program notices

The AR designation has several key features:

- Narrow in scope. It only applies to the specific program for which it was filed. An AR for Medi-Cal does not cover SNAP; each program requires its own form.

- Fast. The form is one or two pages, signed by both the recipient and the AR, and typically processed within a few business days.

- Free. No agency charges a fee to file an AR form.

- No legal authority outside the program. The AR cannot access bank accounts, sign real estate documents, make medical decisions, file taxes, or enter contracts on the recipient's behalf.

One important exception: integrated state portals — such as California's BenefitsCal and Kentucky's kynect — allow a single AR form to cover all programs administered through that portal.

When the AR Designation Is Enough

For the ongoing work of keeping a parent enrolled in their benefits, the AR designation handles nearly everything:

- Logging in to the parent's state benefits portal

- Viewing the renewal calendar and receiving renewal notices

- Gathering and uploading supporting documents

- Submitting completed renewals

- Calling the county caseworker with questions

Year after year, an AR can manage the full annual renewal cycle without ever needing a POA. The AR can also submit new applications for programs like Medicare Savings Programs, In-Home Supportive Services (IHSS), or LIHEAP on the parent's behalf, and receive the eligibility decision.

For most families, the AR designation is the workhorse tool — and it can be in place within days of deciding to help.

When a Power of Attorney Actually Becomes Necessary

The POA is the right tool when the agent needs to act in areas the AR designation does not cover. Common situations include:

- Closing or managing a parent's bank account

- Selling a parent's home or other property

- Signing a contract for assisted living placement

- Consenting to or declining a medical procedure

Without a POA in these situations, the only alternative is a court-appointed conservator or guardian — a process that is significantly more expensive and slower.

A healthcare POA or advance directive becomes especially critical before any major medical event. Hospitals routinely ask for a healthcare proxy on file before surgery or ICU admission.

Note: The Social Security Administration has its own separate designation called Representative Payee for managing Social Security benefit payments on someone's behalf. This is a third, distinct tool — separate from both POA and AR.

A Common Misconception That Trips Families Up

Many adult children assume that having a POA automatically grants AR status for benefits programs. It does not.

Most county Medicaid offices will accept a financial POA as evidence of authority, but they still require the standalone AR form to be filed for the case record. Going the POA route alone — without filing the AR form — often results in caseworkers refusing to discuss case details, and renewal notices going only to the recipient.

The reverse is also true: AR status for one program does not transfer to another. An AR designation for Medi-Cal does not authorize action on a VA pension claim. Each program's form must be filed separately with that program's agency.

The exception, again, is an integrated state portal. In California (BenefitsCal) and Kentucky (kynect), a single AR form covers the full portfolio of programs administered through that portal.

The Recommended Sequence for New Caregivers

For an adult child stepping into a caregiver role, a practical two-step sequence works well:

- First two weeks: File the AR designation with the parent's state benefits portal. This puts the caregiver in position to manage benefits work immediately — no attorney needed, no waiting.

- Second month: Schedule the attorney appointment to prepare a financial POA and healthcare advance directives. These complete the picture for situations the AR cannot cover.

Skipping the AR form and going straight to POA leaves the caregiver locked out of the benefits portal for weeks while legal paperwork is drafted. And even after the POA is signed, the AR form still has to be filed before the caseworker will recognize the caregiver. The POA-first approach costs time and money with no operational benefit.

Always confirm program-specific requirements directly with the relevant agency, as rules can vary by program and state.

Not legal or financial advice. The agency makes the final eligibility decision.