June 7, 2026 · 4 min read

Moving a Parent Across State Lines: What Happens to Their Benefits

When an aging parent moves to a new state, some benefits follow automatically — others restart from zero, and a few disappear entirely. Here is what families need to know before the moving truck pulls out.

Key takeaways

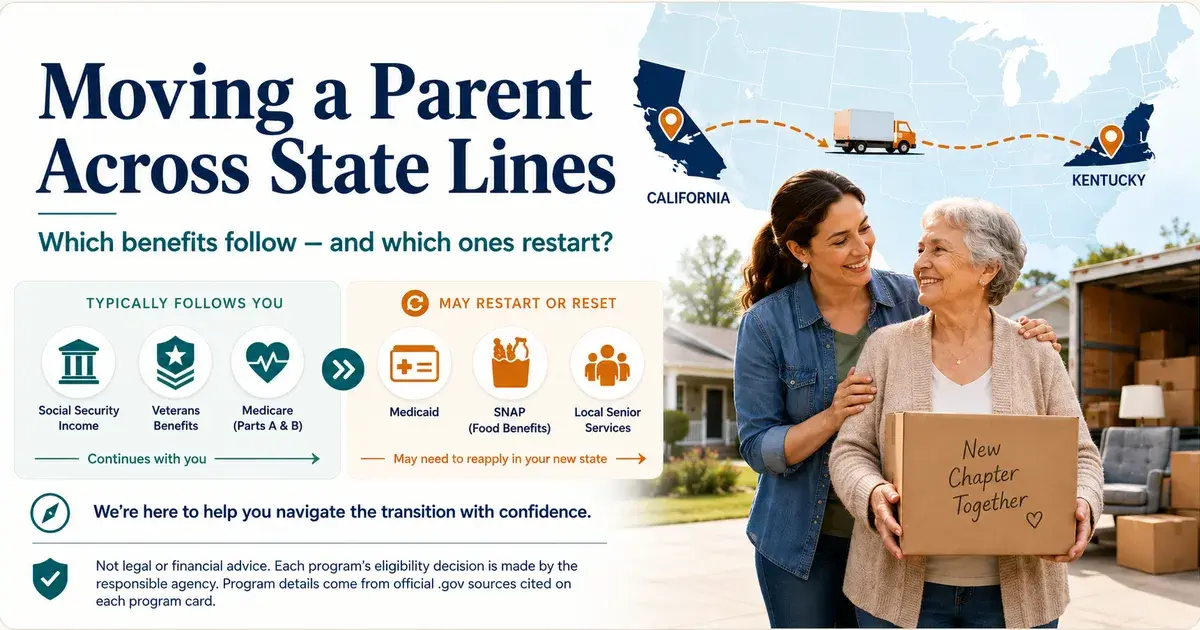

- Federal programs like Original Medicare, Social Security, and VA benefits follow a senior to any new state with just an address update.

- Medicare Advantage and Part D plans are region-specific — a move triggers a Special Enrollment Period to pick a new plan in the new state.

- State Medicaid programs do not transfer; a fresh application is required in the new state, and old coverage should stay active until new coverage is approved.

- SNAP, LIHEAP, and other federally funded but state-administered programs all require a new application in the new state.

- State-specific programs — like California's CARE energy discount — may have no equivalent in the new state, meaning that benefit is simply lost.

- County-level senior services reset completely; the first step after a move is finding the Area Agency on Aging that serves the new address.

The Simple Rule of Thumb

When an aging parent moves across state lines, benefits do not all behave the same way. The easiest way to think about it:

- Federal programs follow the parent to any state with little more than an address update.

- State-administered programs almost always restart — a fresh application is required in the new state.

- County-administered programs reset completely.

Knowing which category each benefit falls into — before the move — is the difference between a smooth transition and a months-long coverage gap.

Federal Benefits That Follow Automatically

Original Medicare (Parts A and B) works in every state and every county. A senior moving from California to Kentucky keeps the same Medicare card and does not need to re-enroll. Updating the address with the Social Security Administration (SSA) takes care of both Social Security and Medicare records at the same time.

Social Security retirement and Social Security Disability Insurance (SSDI) also follow across state lines. An address update is the only required step.

Supplemental Security Income (SSI) follows too, but the move must be reported within ten days. Some SSI rules — including state supplemental payments — vary by state, so the monthly amount may change.

VA benefits — including VA disability compensation, the VA pension, and the Aid & Attendance supplement — follow the veteran or surviving spouse to any state. The address update goes through the VA separately from SSA. VA healthcare access is reassigned to the nearest VA medical facility in the new state.

Federal Benefits That Follow but Need a Regional Reset

Medicare Advantage and Medicare Part D plans look federal, but they are sold by private insurers and cover specific counties or service areas. A Medicare Advantage HMO in Los Angeles County will not have a provider network in Jefferson County, Kentucky. A Part D plan sold in California may not be available in Kentucky at all.

Moving to a new state opens a Special Enrollment Period — typically the month of the move and the two months that follow. During this window, the parent can switch to a Medicare Advantage or Part D plan available in the new state. Missing this window means waiting until the next annual open enrollment period (October 15 through December 7) to make a change.

Medicare Savings Programs — the benefits that pay Medicare premiums and cost-sharing for lower-income seniors — are run by each state's Medicaid office. The federal eligibility rules are the same everywhere, but a move requires a fresh application in the new state. Coverage can resume without much delay, but the paperwork must be filed anew.

State Programs That Restart from Zero

Medicaid is the biggest one. State Medicaid programs do not transfer. A senior moving from California to Kentucky cannot keep Medi-Cal; they must apply for Kentucky Medicaid in the new state. The two programs have different income and asset rules, different application processes, and different renewal calendars.

Important: Keep coverage in the original state active until the new state's Medicaid is approved. Report the move to the original state's Medicaid agency and ask for the case to close on the date the new state's coverage begins — not the date of the physical move.

SNAP (food assistance) is federally funded but state-administered. The case from the original state is closed and a fresh application is filed in the new state.

LIHEAP (energy assistance) works the same way — state-administered, sometimes county-delivered, and a full restart is required. Application calendars vary by state, so timing the move can matter.

State-specific programs — cash assistance, pharmacy assistance, property-tax relief, and senior nutrition programs — all restart in the new state. Some have direct equivalents (CalFresh and Kentucky's SNAP are both the same federal program). Others have no equivalent at all. California's CARE energy-bill discount does not exist in Kentucky. Kentucky's veteran property-tax exemption does not exist in California. Those benefits are simply lost or gained depending on the direction of the move.

County Programs Reset Completely

Every state organizes county-level senior services differently, and the reset is total. The Area Agency on Aging in the new county is a different organization from the one in the old county. Home-delivered meals, senior transportation, county property-tax assistance, and county-administered general assistance all require fresh enrollment.

In some states, each county runs its own programs independently. In others, counties are grouped into multi-county regions that share an Area Agency on Aging. The first step after a move is finding out which agency actually serves the parent's new address. A call to the new state's department of aging — or a visit to the state's senior services website — is the way to identify it.

The Question Worth Asking Before the Move

For families weighing a cross-state move, the right question is not simply "which state has lower taxes?" It is: which specific benefits restart, which disappear entirely, and what is the net change in the parent's annual benefit picture?

The answer is concrete and can be calculated. A parent moving from California to Kentucky, for example, would lose California-specific programs and gain Kentucky-specific ones. Federal benefits stay the same. The net annual benefit value can go up, down, or stay roughly flat — it depends on the parent's specific eligibility profile.

Running this comparison before the move — not after — gives the family time to plan for any gaps and to file new applications as early as the new state allows. Always confirm current eligibility rules and application requirements directly with the responsible agency in the new state, as program details can change.

Not legal or financial advice. The agency makes the final eligibility decision.