July 8, 2026 · 4 min read

4 Tax Law Changes for 2026 Every Retiree Should Know

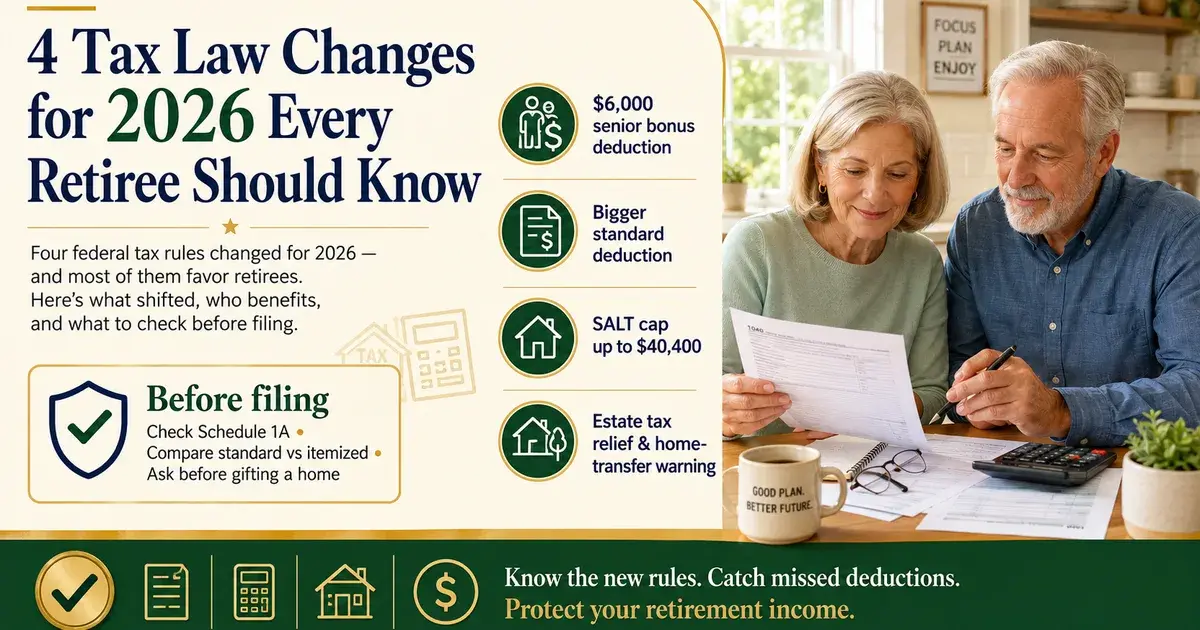

Four federal tax rules changed for 2026 — and most of them favor retirees. Here's what shifted, who benefits, and what to check before filing.

Key takeaways

- Americans 65 or older get a new $6,000 senior bonus deduction for 2025–2028 — on top of the regular standard deduction.

- A married couple both over 65 can now shield roughly $47,400 of income before federal taxes apply.

- The state and local tax (SALT) deduction cap jumped from $10,000 to $40,400, but only helps those who itemize.

- The federal estate tax exemption is now set around $15 million per person, but state estate taxes can start much lower.

- Transferring a home to a family member while alive can trigger a large capital gains tax bill — waiting until death resets the tax basis.

- Tax software may miss brand-new line items like Schedule 1A in its first year — confirm the senior bonus deduction was applied.

Why 2026 Is a Unusually Good Tax Year for Retirees

Four federal tax rules changed for 2026, and most of the changes favor people over 60. No notice arrived in the mail. The rules simply shifted.

Middle-income retirees stand to benefit the most — and are also the most likely to miss these changes entirely. Tax software and busy preparers can overlook brand-new line items in their first year. Knowing the rules is what allows someone to catch a mistake before it costs them money.

A quick note: This article is educational and based on current 2026 tax rules. Confirm specific numbers with a qualified tax professional before filing.

Rule 1: The New Senior Bonus Deduction

This is the change most likely to go unclaimed, because it has a name almost nobody recognizes yet: the senior bonus deduction.

From 2025 through 2028, every American who turns 65 or older by the end of the tax year receives an extra $6,000 deduction — just for being 65. That's the entire qualification. If both spouses are 65 or older, each gets $6,000, for a combined $12,000 off taxable income.

This deduction is separate from the regular standard deduction and the longstanding extra senior amount. It stacks on top of both. No itemizing is required, and no receipts are needed. It appears on a new form called Schedule 1A — a form that did not exist on tax returns two years ago and that some tax software may skip if it hasn't been updated.

Income limits apply. The deduction begins to shrink once income passes:

- $75,000 for a single filer

- $150,000 for a married couple

It disappears completely at $175,000 (single) or $250,000 (married). A retiree living on $58,000 a year in pension and Social Security income gets the full amount.

One more connection worth knowing: this same income figure also affects Medicare premiums two years later. Crossing certain income thresholds — even by one dollar — can cause premiums to jump for the entire year. One number, two separate bills.

Rule 2: The Bigger Standard Deduction Stack

The basic standard deduction also grew for 2026 — roughly $16,100 for a single filer and $32,200 for a married couple.

On top of that, anyone 65 or older still gets the longstanding extra senior amount — roughly $2,000 for a single filer. Add the new $6,000 bonus deduction, and a single retiree over 65 can now shield approximately $24,150 of income before federal taxes apply. A married couple, both over 65, can shield around $47,400.

This matters especially for retirees because many people over 65 live right around or below those amounts. For a significant number of them, this stacked deduction means a portion of their Social Security income stops being taxed at all — because total taxable income falls below the threshold where that tax kicks in. That's real money every year, with no special action required.

Rule 3: The Bigger State and Local Tax Cap

This change received the most news coverage — but it helps fewer retirees than headlines suggest.

For years, there was a hard $10,000 cap on deducting state income tax and property tax combined. For 2026, that cap jumped to $40,400.

The catch: this only helps someone who itemizes deductions. And itemizing only makes sense when total itemized deductions — property tax, state income tax, mortgage interest, charitable giving — add up to more than the stacked standard deduction. For a married couple over 65, that bar is roughly $47,400.

Consider two different retirees:

- Patricia and James in New Jersey pay $18,000 in property tax and $22,000 in state income tax — $40,000 total. Under the old rule, only $10,000 counted. Under the new cap, all $40,000 counts. This rule saves them real money.

- A retiree with a modest paid-off home and low state taxes will likely still come out ahead taking the standard deduction. The new $40,400 cap never touches their return.

The same rule produces two completely opposite outcomes depending on the situation. Knowing which category applies is the key step.

Rule 4: Estate Tax Relief — and the Trap Next to It

The fourth change is the quietest, and it lifts a real worry — but only for a narrow group.

For 2026, the federal estate tax exemption is permanently set at around $15 million per person ($30 million per couple), rising with inflation. For the vast majority of retirees, the federal estate tax is simply not a concern.

But two things sit right next to that relief that often go unchecked:

State estate and inheritance taxes. Several states charge their own estate or inheritance tax, sometimes starting as low as $1 or $2 million. A paid-off home plus a lifetime of savings can quietly reach that level.

The step-up in basis — and the trap of gifting a home too soon. When a homeowner passes away and leaves a home to a family member, the home's tax value resets to its current market value. All the growth built up over decades is wiped clean for tax purposes, meaning little to no capital gains tax if the heir sells.

But if that same homeowner signs the house over to a family member while still alive — trying to be helpful — the family member inherits the original purchase price as the tax basis instead. When the home is eventually sold, capital gains tax could apply to the entire difference between the original price and the sale price. One well-meaning decision can cost a family tens of thousands of dollars. The tax code rewards waiting, and a qualified estate planning professional can explain the options.

What to Check Before Filing

These rules are written into law and available to anyone who looks. The challenge is that the tax system is not designed to explain what filers are owed — only to collect what they owe.

Before filing this year, a few steps are worth taking:

- Add up total income — pension, Social Security, retirement account withdrawals — and compare it to the senior bonus deduction income limits.

- Ask a tax preparer or check tax software specifically about Schedule 1A and the senior bonus deduction. Don't assume it was automatically applied.

- Compare itemized deductions to the stacked standard deduction to determine which is larger.

- Before transferring a home to a family member, consult a tax or estate planning professional.

The most useful question to bring to any tax appointment this year: Am I claiming every senior deduction available on this return?

Not legal or financial advice. The agency makes the final eligibility decision.